I go to Flame University every year to teach undergraduate students a course called “FINC362: Case Studies in Business and Investment Analysis.” These case studies are based on real businesses; sometimes, the coverage is real-time.

In early 2022, while delivering this course, I devoted class sessions 15 to 18 to two cases on investing in listed, government-owned businesses. One of the cases was on Cochin Shipyard (CSL).

In this post, I am reproducing what was presented in the class based on an earlier note I had prepared in 2020 on this business. A lot has happened in this company since the note was written. For example, the company delivered INS Vikrant to the Indian Navy, India’s first indigenously built aircraft carrier. Then COVID-19 came, causing a delay but not a loss of revenue and earnings. There were some other important developments in the business as well. None of them are covered in the note. Also recently, the company did a stock split for which I have not made any adjustments in this post.

As of this writing, my firm’s clients are invested in this stock. Nonetheless, this is not a recommendation to own this stock, nor was it during the presentation of the case. The business model of this company is unique. I presented it to my students so they could learn from studying it in some detail.

Cochin Shipyard’s Business Model

CSL owns the only shipyard in India that can build ships up to 1,10,000 DWT (deadweight tonnage). It’s the only shipyard in India to repair vessels up to 1,25,000 DWT and the only yard to repair an air defence ship.

Over the years, CSL has undertaken dry dock repairs of Aircraft Carriers INS Viraat and INS Vikramaditya. The company can also undertake complex and sophisticated maintenance to all vessels, including oil rigs, naval and Coast Guard vessels, offshore vessels, dredgers, fishing vessels, passenger ships, port crafts, and other merchant vessels.

Besides the aircraft carriers, CSL also builds vessels for the Indian Navy and boats for the Indian Coastguard. And because CSL is one of the two shipyard companies in which the Indian Government has a majority stake (the other one is Mazagon Dock), it gets preferential treatment for orders from the Indian Navy and Indian Coastguard.

Given that India has a coastline of about 7,500 kilometres, both the Indian Navy and the Indian Coastguard need a large number of ships. The company is also benefiting from increased spending by the Indian Government on massively expanding India’s defence capabilities. CSL has a healthy and growing order book, which provides high visibility on revenues and earnings.

Attractive Features of CSL’s Business Model

One, CSL’s business is non-cyclical, even though it’s in the shipbuilding and repair business. That’s because only 30% of revenues are from non-government customers.

As the above table shows, in only one year (FY12), the company’s revenues and earnings fell out of the last ten years.

Typically, shipbuilding is a hugely cyclical business, just as the commercial shipping industry is. However, CSL’s business is not cyclical. That’s because it has minimal exposure to the business of making commercial ships like bulk carriers and oil tankers. Instead, most of its shipbuilding business (70%) comprises building vessels for the Indian Navy and Indian Coast Guard. This includes a hugely prestigious project of building India’s first fixed-wing aircraft carrier, INS Vikrant. This project will put India on a list of eight countries capable of manufacturing aircraft carriers.

Two, CSL businesses earn high returns on equity without employing any debt. Over the last seven years, annual pre-tax ROE has ranged from 23% to 26%. That’s more than twice the AAA bond yields of 10% annually. In none of these years, there was any net debt on CSL’s balance sheet.

Third, CSL has consistently earned excellent and stable profit margins over the last 10 years. This is not a low-margin-high-ROE model where exceptionally high capital turns cause high ROE. A low-margin business is vulnerable to margin contractions even if it delivers a high ROE. This is not the case with CSL. That’s because its margins are protected.

Fourth, CSL’s revenues and earnings have been on a solid growth trajectory for the last many years, a trend will continue because of the growth in its order book, which translates into rising revenues and earnings.

As of the end of December 2019, CSL’s order book size was INR 152 billion, equivalent to roughly four years of revenues. Here’s the break-up of its current order book.

There is a high degree of visibility about CSL’s future revenues and earnings, which is a favourable factor.

The current Indian government spends far more on defence than previous governments. Two of CSL’s largest customers — The Indian Navy and the Indian Coast Guard — have significantly increased their capex plans over the last few years, as the table below shows.

For CSL, these capex plans translate into an order book, which converts into revenues and earnings over time.

Five, apart from orders for building new ships, CSL has expanded its ship repair business over the last few years. Revenues in this vertical have multiplied by 3x over the previous 5 years, representing 18% of its annual revenues. The repair vertical is not only a non-cyclical, repeat business, it’s also highly profitable. EBIT margins in this business (25% a year) are significantly higher than in the shipbuilding business (20% EBIT margins). I particularly like that the existing fleet of ships manufactured by CSL will provide long-term repeat business to its repair vertical.

The company has also embarked on an expansion plan that will produce new sources of revenue and earnings in the coming years. See, for example, the table below, which highlights these plans.

Six, many of CSL’s competitors in the private space have gone out of business over the last few years. In 2018, the shipbuilding capacity was as follows:

Of these, several competitors have shut down or are under bankruptcy. These include ABG Shipyard, Bharti Defence and Reliance Defence. These developments benefit CSL as the industry’s competitive intensity is reducing. Even without this reduction, CSL, being a government-owned company, gets preference for orders from the Indian Navy and Indian Coast Guard.

Seven, a substantial part of CSL’s revenue is derived from customer contracts, which protect CSL’s profit margins from cost escalations. Since many of the contracts are for unique vessels (like aircraft carriers) where capability and quality are the focus and benchmarking is difficult, cost escalations, if any, are borne by the customer. This is very important from a structural point of view because if the company fixed the price of ships to be delivered five years from now without any price escalation clauses in its contracts, that would be an accident waiting to happen.

I also like that CSL’s labour costs are not only low compared to competitors (see chart below) but also have an element of flexibility. That’s because roughly 60% of the people employed at its facilities are temporary workers. This means that even a significant slowdown in orders (which I think is unlikely) will not hugely impair its profit margins. A flexible cost structure is a sign of a robust business model.

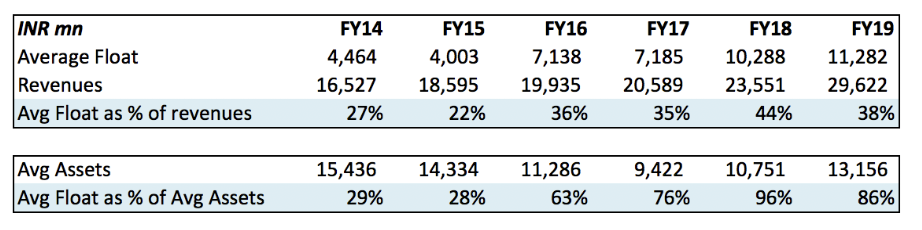

Finally, many of CSL’s major customers make up-front payments to the company to execute the contracts awarded to it. This “float” — significant interest-free advances from customers (see table below) — is a beautiful form of financing and a sign of the strength of the company’s competitive position.

Overall, I think that CSL possesses several markers of a high-quality business — non-cyclicality, high ROE, zero debt, excellent and stable profit margins, strong growth prospects including several new sources of earnings, reducing competitive intensity in the industry, cost-plus contracts which protect margins, flexible labour costs in a labour-intensive industry, and the presence of significant and growing float from customers.

Usually, when one sees this combination, one would expect the market to highly value such a company. Is that the case with CSL? The answer is no! I will discuss this in the valuation section of this document, but before I do that, I would like to share my thoughts on the quality of CSL’s management team.

Excellent Management

CSL is run by a team of highly motivated and competent managers. The average experience of CSL’s critical management team is more than three decades (the CEO has been with the company since 1988), indicating high loyalty and commitment, low attrition, improved skills, understanding of complex jobs, and increased productivity.

Additionally, CSL has not witnessed a single workers’ strike in the past 25 years. This is significant because shipping building and repairs are capital intensive, and CSL operates primarily out of Cochin, in Kerala — a state famous for its communist governments and worker strikes.

CSL has also received many awards for excellence, including the prestigious “excellent” report from the Corporate Governance Grading Report of CPSEs (Central Public Sector Enterprises) for 2018-19.

CSL’s Stock is Ridiculously Cheap

At INR 259 per share, the company is valued by the market at INR 34 billion. Estimated pre-tax earnings for FY20 are INR 9 billion. The pre-tax P/E multiple is just 3.8x, and the pre-tax earnings yield comes to about 26%, more than twice the prevailing AAA bond yield of 10% a year.

Given that earnings have grown at an annual average growth rate over the last five years at 20% and given that I expect the earnings to continue to grow at a similar rate over the next several years, one is getting an opportunity to buy into this excellent business at a valuation where one is not paying anything for growth.

The stock is also cheap in asset value. The current estimated book value per share is INR 274. At INR 259 per share, the Price-to-book value ratio comes to just 0.9x. The dividend yield is also excellent at 6%.

Hello Sir,

I think most of the people would have laughed at this post when PSU’s were untouchables, but today no body can dare to do so when price is up 6X.

Still I will play devil’s advocate here.

And how do I dare to do so, One, prestigious project INS Vikrant:

The primary driver for huge revenue visibility , high profit margins and high ROE for years had been the project INS Vikrant which was also one of the biggest in terms of Order Size. But that those golden days are not going to repeat.

Based on management talks in past concalls:

“You will not get a margin like an IAC anywhere and we have continuously mentioned this, the kind of EBITDA margins will not be available in the shipbuilding business”

“Now margins, these are all competitive tenders, the ASW and the NGMV. We actually said that

the ASW Corvette was extremely competitive fought contract and the margins we had

conveyed earlier, the margins are actually in single digit levels over there”

Two, its still a PSU and when Hindustan Aeronautics has to borrow money in past to pay salaries because Navy was not paying its dues, it can happen with any other PSU:

https://timesofindia.indiatimes.com/india/broke-hal-borrows-1000-crore-to-pay-salaries-to-employees/articleshow/67390881.cms?from=mdr

Nevertheless, buying into Cochin Shipyard at the time of your post still made ample sense as all the risks were covered in the dirt cheap price.

But I will argue that Cochin Shipyard is touted as Growth Stock today which is scary to me.

[…] Strategic Insights on Cochin Shipyard – Cochin Shipyard’s robust and non-cyclical business model, high returns on equity, strong order book, skilled management, and undervalued stock position it as an attractive investment opportunity in India’s shipbuilding industry. Read here. […]

Sir.

I worked in a PSU a long time ago, wherein the culture was not to work ( for the employees), which made me quit and join the private sector. I hardly see any cultural change there. I always remember MTNL, the jewel, which seems to be different today, There seems to be too much hype around PSU, which would stand corrected in time, by the Markets.

Sir it would be preferable if you also show the negative side or why you also belive one should not invest in the company i.e both side of coins.