After doing a series of posts on this subject, recently, I presented my thoughts to students at MDI. That presentation can be downloaded from here and the slides along with my commentary are reproduced below.

I practice what I teach and I teach what I practice.

After doing a series of posts on this subject, recently, I presented my thoughts to students at MDI. That presentation can be downloaded from here and the slides along with my commentary are reproduced below.

Comments are closed.

Professor, can you please provide a video of this lecture to go along with the presentation or provide a written explanation of what were you explaining with the slides? Thank you very much.

There is no video and what I spoke is at the bottom of each slide.

Thanks

Professor, Is the float same as Negative Working Capital? Dell has been quite famous for this.

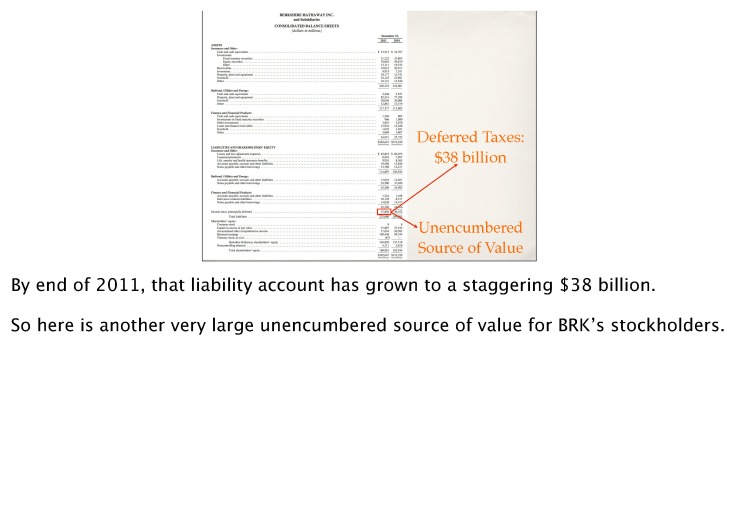

Partly true but as explained in the presentation, there are forms of float other than negative working capital. Deferred taxes for example.

What a treasure this presentation has been…Its like reading the mind of buffet inside out…Thanks professor for such an amazing wisdom dose.

Vikas Kukreja

[…] read post from Fundoo Professor about how Buffett discovered the importance of […]

Prof bakshi

If we use the concept presented above to banks, a well run retail bank with stable and low cost deposit base also has ‘deposit float’. if the bank (such as HDFc) can lend (asset side) conservatively and sensibly, then it is a great business.

I guess that explains the comment which buffett has made about wells fargo and Bank of america, that the value is in their deposit base and banking is a simple business if done conservatively

rgds

rohit

Agreed. Floats in banking are probably the biggest source of floats in business but because they come with other forms of onerous leverage plus a lot of stupidity on the other side of the balance sheet, they are quite different qualitatively than floats in debt-free companies having solid moats. That’s my view.

There seems to be some typo on the EIL slide. The ‘Security deposits +advances received from clients+ income received in advance’ are closer to Rs 630 cr and not Rs 6,150 cr.

Such a focused discussion on floats is truly a treat as evaluating the value of a float in a particular situation is always tricky and one can easily have a fuzzy understanding of it and not know about it.

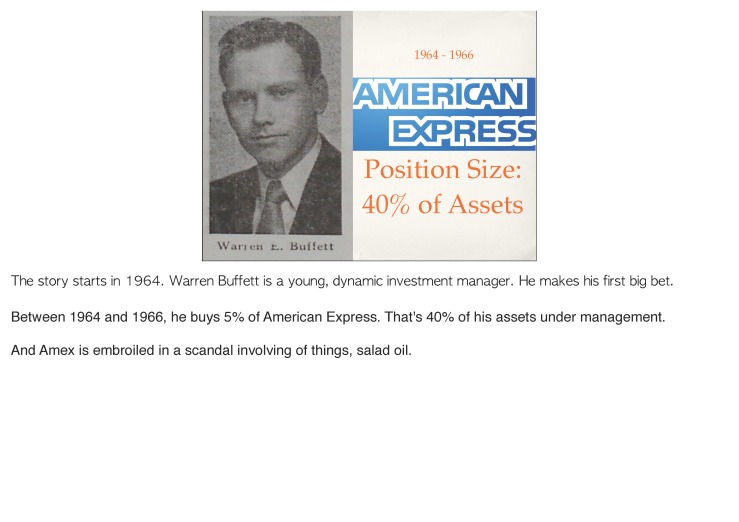

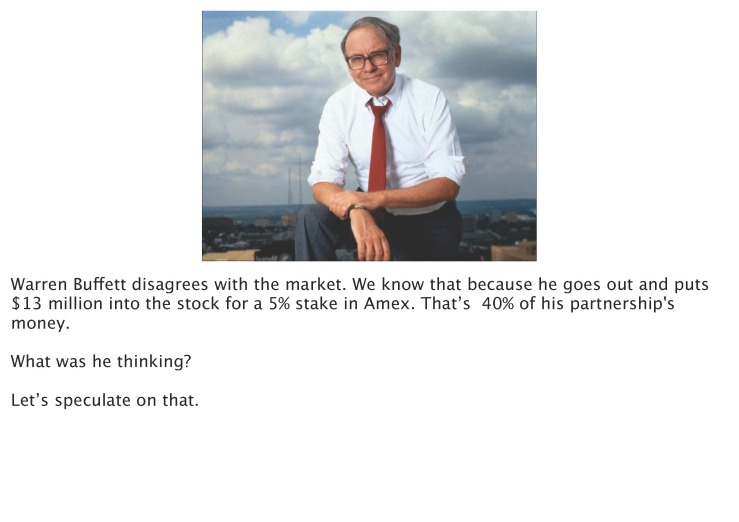

One point though. As for the Amex situation discussed in the presentation, what would be the implications of the fact that the $150 m of loss due to the scandal completely wiped out Amex’s entire equity (and then some) of $84 m as at year end 1964 as shown in the slide?

This also highlights another fact about such high degrees of leverage in relation to equity capital. And that is that even though the float may carry zero interest, may not need any collateral and may be a revolving fund, it is still an outside liability. So if its scale is very large relative to equity capital, any loss while employing that float, even if moderate in relation to the size of the float itself, may turn out to be extremely large in relation to equity. So wiping out, say, 50 years of carefully built up equity in a single year may easily occur if one is not extremely careful while investing/employing the assets bought out of that float. Which is interesting because a company whose core business generates high amounts of float, by definition requires very little capital to be employed its core business. So as the core business grows, it generates higher and higher absolute amounts of float. And all that float money that’s generated is not required in the core business itself. So what does the company do with that float money? Come to think of it, most companies are quite severely constrained in employing that float. Because their expertise and moat lies in their core business. And that core business doesn’t require that float money. So for such companies, there lie only 2 options.

1. Invest the float in plain vanilla instruments like short term government bonds and bank deposits which offer measly returns but also carry no risk and require no expertise.

2. Try their hand at employing the float money in other areas where the company doesn’t have the level of expertise and experience that it has in its core business. And by virtue of that significantly lower level of expertise in such other ventures, face the earlier cited risk that incurring even a moderate loss on such other adventures may prove catastrophic in relation to equity capital.

So unless you have someone like Buffett on board, who’s very expertise lies in being able to continually find newer avenues to invest the float money without straying from his core field of expertise, most companies that generate float due to a moat would have to logically restrict themselves to option number 1. And thus investing that float into ‘highly productive assets’ is out of the question for most businesses that generate it.

So for most such companies without Buffett, the value of the float generating capability of the company to the shareholder of that company comes down to just two things – 1. The exceptionally low levels of equity capital required to run the core business, and 2. The excess post-tax earnings that are generated by way of interest earned on investing the float in low return AAA debt instruments.

While it seems that this applies to all float generating companies without a Buffett type capital allocator, it applies even more so to such companies in a cyclical business where the float comes and goes along with the business cycle and thus can’t be treated like a revolving fund in the first place (BHEL for example).

Taha, that’s wasn’t a typo. It was a stupid mistake on my part. Thanks for pointing it out. I have fixed it.

As for your other points, there is an option 3 which is the option to withdraw cash from the business. Take a look at the slides on Amazon.com, or better still download it from here

Amazon.com, if it so chooses, can withdraw cash from the company and deposit it in the pockets of its shareholders. Notice that the float accounts exceed investment in inventories, receivables and fixed assets. Since float exceeds operating assets, the company’s stockholders have negative investment in them. This is evident from the huge treasury assets of $9.5 billion. The stockholders have “no skin in the game” in you think of “game” as “operating assets”

So long as the trust in amazon.com’s reputation is maintained in the minds of customers and suppliers (who taken together are funding all the operating assets of the company), the stockholders can enjoy an infinite return on their investment.

Other that that, I agree with your analysis that the weak link in such business models is the trust factor. But if the stockholders have no skin in the game, and they enjoy the benefits of a free float for a long time, they have little to lose, isn’t it?

Thanks

I don’t think an Amazon would or should take Option 3 of withdrawing the excess float cash ($9.5 b) from the business and paying it out to shareholders as dividends (and thus operate on negative or nil equity in the core business). That’s because if it were to do so, it would then make the company’s capital structure quite risky, as it would then be unable to withstand any temporary declines in business or even the occasional unforeseen shock that is quite likely to hit even the strongest of businesses every once in 20-30 years. Because a decline in the level of business may directly lead to a decline in the level of float. And even if this decline is temporary, and if the company is in a position where it is funding all its operating assets from current liabilities with no margin over that, it will not be in a position to operate with a reduced float. Operating with such a precarious capital structure may also work negatively for the ‘trust factor’, and thus ensure that the very reason why it has this float – trust from supplier and customers – may not be there anymore.

Out of the accounts payable and accrued expenses of about $15 billion, it is already using about $5.5 billion to fund operating assets and the rest of the $9.5 billion of those liabilities are lying as cash and liquid securities. So in other words, the rest of the money from the float is lying as a buffer or margin of safety to absorb any unexpected declines in the level of float. So I think it needs to be there.

Also, if they were to payout to stockholders the $9.5 b, yes the stockholders would then have no ‘skin’ (equity) in the ‘game’ (operating assets). But if things were to go sour, even though they would then have nothing to lose in the form of no equity capital invested in the company, they would have a lot to lose in the form of the $115 billion of market cap that the company enjoys, which they should rightly consider to be the value of their current investment in the company.

Imagine someone buying the whole of Amazon right now. At the current market price, he would have to pay $ 115 billion. I don’t think he would put the value of his investment, i.e. $115 billion at risk for the prospect of removing just $9.5 billion of other people’s money from the company. Because his skin in the game would not be the level of equity invested in the company but rather the $115 billion. He would indeed have a lot to lose. It would be like killing the golden goose in trying to get all the golden eggs at once.

He would have nothing to lose only if the company’s common stock was for some reason valued at significantly lower than $9.5 billion. He could then remove the $9.5 billion of cash (other people’s money), and continue to have a call option on the potential future success of the then speculatively capitalized company, without have anything to lose.

Excellent points Taha. Amazon.com should not withdraw money represented by float – at least not in one shot. That — as you have argued persuasively — will be bad for stockholders.

The value of a firm is the present value of cash that can be be taken out of it over its lifetime. Here, let’s differentiate between “can be” with “should be.” For example it isn’t dividends that determine value; its “dividend paying capacity.” And dividend paying capacity exceeds reported earnings frequently enough to warrant attention.

Rise in float for amazon.com would be represented by the difference between cash flow from operations before working capital (Let’s call that “A”) changes and cash flow from operations after working capital changes (“B”). B will exceed A year after year if float increases. When you calculate owner earnings, you’ll find that economic earnings exceed reported earnings every year because B exceeds A. And for valuing amazon.com – or any business – you should discount economic earnings and not reported earnings.

Amazon.com should not withdraw the excess of B over A – but it could if it wished. It could do so slowly paying out more than what it earns. If it did that it would be paying out float (other people’s money) to its owners while that balance in the accounts represented by float kept rising (growth in float offsetting withdrawals).

Write to me at sanjay@sanjaybakshi.net and I will send you a case on a company which demonstrates very persuasively that negative reported equity is not a big deal.

Prof. Bakshi,

Pardon me if the question is too simple-minded: Your first slide says that floats & moats are two separate ideas. But didn’t you drive home the point in your original posts on the subject that a moat is actually one among many types of float?

I had taken pdf printouts of your original posts, underlined the key concepts and made the following notes:

TYPES OF FLOATS

1. Insurance Premia

2. Deferred taxes

3. Travellers cheques

4. Current accounts

5. Premia on writing derivatives

6. Market Power – Moats:

(a) Advances & deposits

(b) Trade credit

BENEFITS OF FLOATS

1. High ROIC

Thanks.

Satyajeet, they were two different ideas on slide 1 and then they gradually came together in later slides.

My argument in the presentation is that float comes in many forms and if there is a solid moat its quiet likely there will be a low or zero cost float as well. If I am right, then there is a quantitative way to spot a moat – just measure the size of float and its trend over time…

I just find it useful to look at the world of business from the float point of view.

some gold jewellery companies offer a financing scheme where they collect money every month and then at the end of 12 months (years?) folks can buy gold. this could also be a type of moat. what do you think?

a little question about derivatives.. at what point and by which means ( valuation techniques ) a retail investor can/should create float

……. considering derivatives are traded in open market and people with small cap. ( students ) may want to get some capital at low cost

I am not in favor of using derivatives to produce a float for people with small cap or any cap for that matter. What Mr. Buffett has done with derivatives is not likely to be replicated by most people. I used the example of derivatives just to illustrate that Mr. Buffett has used the idea of float in many way in his career.

In my view, the best form of float for someone who wants to be a value investor to manage other people’s money for a profit share or to invest in businesses at attractive prices using float at attractive prices.

Thank you Sir !!

Although I would like to know, why it would be hard to replicate

……or it is excluded because of opportunity cost ?

additional question 😀 as you are a NNT fan boy ……. do you buy out-of-money options ? …… if somebody want to know more about derivatives as value investment instruments, which reading material you would refer, to increase our understanding of this topic ? Please

No I don’t buy out-of-the-money options from traded option markets. But when you invest in value, you often create free lottery tickets which are, in effect, free options. If you buy a growth stock at a price which implies a a negative or much lower growth rate than what you anticipate, you’ve acquired a free call option on growth. Likewise, if you can buy a debt-free company for less than its debt capacity, you’ve paid a price equivalent to a “bond component” embedded inside the stock which has claim on only a part of the cash flow; you’ve acquired a claim on the rest of the cash flow for nothing…

Dear Professor,

Can you please help us understand the following?

Mr Buffet’s businesses enjoying floats have to sweat the floats. Any surplus cash they generate and not use it effectively has to be returned to Berkshire.

In case of EIL

1 It has high RONW business.

2 It enjoys float.

But it has bank deposits worth 1500 Crs over the last several years. Doesn’t this water down the advantage of Free float it enjoys?

Prof. Bakshi,

One could read Security Analysis and Buffett’s letters thrice, and still not even come close to what you teach. Clearly, what you write is a higher level synthesis or a deeper interpretation of the masters.

For example, made an inventory of some additional concepts from this post & comments:

1. A perpetual current liability or consolidated account of sundry balances = Revolving fund = A respectable Ponzi scheme.

2. Manage other people’s money at a profit share = A form of float.

3. Business using low-cost floats, at an attractive price = A form of float.

4. Track size and trend of float over time = Quantitative way to detect the presence of float.

5. Rise in float = Cash flow from operations after working capital changes – cash flow from operations before working capital changes. (Your exchange with Taha Merchant, especially your reply containing this bit makes my head spin!)

6. Growth stock at an attractive price = Free call option (on growth).

7. Debt capacity bargain = Free call option (on free cash flows to equity).

A question on sophistication/nuances vs. simplicity: What you practice is a sophicated version of value investing. Could some of the same result be achieved by a less skilled investor using a simpler version?

For example instead of measuring or tracking float to detect the presence of moat, could one simply prefer high ROA and ROIC companies? Stalk them for attractive prices + also check out their qualitative characteristics before buying? For example, FMCG companies in 2004-05 or HUL in 2010 at around Rs 220 per share.

It’s a lesson which is apparent from Berkshire letters, which even a beginner can grasp. Would it serve the same purpose? Is deep simplicity at work?

Great post and great discussion (thanks to Taha) as always.

I’m guessing that like any leverage a “business model created” float should cut both ways. Shouldn’t it be a huge drain on cash when the business slows down. It’s easiest seen with a -ve operating working capital business like AMZN. A decease in top line will not only result in GAAP losses (or lower profits), it’ll also result in cash drain as your working capital becomes a little less -ve. “B” will not only not exceed “A” it’ll actually be negative.

Besides with slowing business you might actually lose your bargaining power over suppliers (AMZN), be forced to give better terms to your customers (EIL) or both. This could be a triple whammy (cash drain due to losses, -ve w/c and worsened bargaining position). So the safety of such floats is predicated upon business growth, at least in nominal if not real terms. Ponzi schemes as you pointed out.

I whole heartedly agree with you that a negative equity in itself is not a problem as long as the business is predictable, growing and easily able to service debt. There’s no dearth of decent companies with negative equity (DNB, CLX). It’s the same as being current on their mortgage but have upside-down equity…no dearth of those either now a days!!

Any form of leverage will hurt you if you have to give the money back and don’t have it. So, yes, it’s a double edged sword but its’ edges are blunt as compared to other forms of leverage such as plain vanilla debt where you have to put up collateral, pay interest, and have to return the money by a definite date.

So yes, a de-growth will be a problem but sometime thats hopefully way off – just like death (remember in the long run we are all dead).

Many businesses which have mediocre ROA’s but high ROCE’s caused by the presence of a large and free (or low cost) float will become unimpressive if the float was to disappear. That’s because if float disappeared and the business still has assets employed then the free (or cheap) financing will have to be replaced by onerous debt, or equity. Equity is safest but unfortunately it results in dilution…

So it’s a tradeoff. A “safe” operation won’t be as profitable and an unsafe one which uses leverage will be quite profitable particularly if the leverage is of the highest quality (think high quality floats) and if it can be kept for a long time.

Thanks.

Hi Professor Bakshi,

Thank you for creating and sharing this presentation!

On the 41st slide, you stated that some companies will use financial shenanigans to understate debt by creating large amounts of trade credits (with implicit costs). I was wondering if you can expand on why businesses would do this over simply issuing debt or financing through other conventional methods. Are the costs associated with trade credits less than the other options?

Thanks!

David, camouflaging in the jungle may carry a cost but is still helpful to the camouflager.

In the financial market jungle, the camouflager tries hoodwink analysts who are not trained to look at the “big picture.”

By resorting to an increased amount of trade finance, a business achieves three things: (1) it can use the trade finance to retire debt, so balance sheet reported debt will decline after this type of refinancing is done; and (2) operating cash flow after working capital changes will appear to rise because increased trade credit will reduce reported working capital; and (3) if debt is camouflaged as trade credit then analysts calculating Enterprise Value (market cap + debt) may think the company is cheaper because in calculating EV they may ignore the camouflaged debt.

Analysts who focus on debt/equity ratios will be impressed by the decline in reported debt. Analysts who see the trend in working capital will see it declining and take that as a positive development.

In reality nothing is changing. That’s because trade credit in most businesses comes at a cost. If you pay upfront, you get a cash discount; if you don’t, you wont get any cash discount. So the difference between the price you pay at the end of the credit period and the price you would have paid had you paid now is the implicit cost of financing. Obviously, for a business if interest rates are cheaper on bank borrowing, the business would not want to rely on trade credit because borrowing from bank will be cheaper.

Because trade credit comes at a cost, the act of accessing increased trade credit and using it to retire bank debt will do nothing for economic earnings. That’s because the higher prices the business pays for material purchased would be offset by reduced interest expense on debt retired. So, there won’t be any change in reality. But for some analysts, as discussed above, this would be impressive.

One reason why businesses may resort to expensive trade credit and use the money to retire debt is covenants on bank borrowing. Sometimes a bank may insist that the reported debt/equity ratio cannot exceed a specified ratio, so if a borrower is getting close to that ratio, it may resort to trade financing.

I mentioned above that in most businesses trade credit comes at a cost which should roughly equal the going rate of borrowing money. Most, but not all. Which businesses get trade credit for free or at a low cost? Those who have immense market power – companies like Wal-Mart and Amazon.com. If you’re a supplier to a Wal-Mart, you really can’t say pay me earlier and I will give you a discount because if you did that your low margin will evaporate! So you just have to take the terms Wal-Mart offers you and if you don’t then risk losing it as your largest (or sometimes, your only) customer. It is this market power of Wal-Mart which gives it access to cheap or free trade credit— a float— which helps finance it’s inventories. In the case of amazon.com, this float is so huge that it exceeds not only inventories and receivables but also investment in fixed assets! This means that equity investors have no investment in the operating assets of the firm.

Hi

Enjoyed reading your analysis on float. It really clarified my thinking. Simple question for you? The cash on the balance sheet – should I add that to my enterprise value to get to the equity vaLue. Is that what you mena by unencumbered assets – ie if the float is cheap and enduring, then then assets it funds should be valued at their earnings value. I am always tempted to think that if you have negative working capital/float, and that funds cash to not include the cash in the equity value, “because that belongs to customers or trade creditors” I guess your argument is that if the float is cheap and enduring, then you can count the cash in the equity value.

If the float is free and enduring then, if there is cash on balance sheet which is not needed by the business because of enduring float, then that cash can counted as surplus i.e. unencumbered. In such situations, you can DEDUCT (not add as you wrote) it from the market value of the company (market cap + debt) to derive EV (the market’s assessment of the value of the business.)

Thanks – agree with your analysis, As for deduct vs add. Was simply saying that for a firm with net cash. Once I have taken a view on the enterprise value of the firm. will add the unencumberd net cash on the b/s to get the value of the equity.

Lets say one is looking at the average business, which does not enjoy a genuine float in excess of its current assets, and which has some amount of debt on its books. In such a situation, how does one know if the company is understating the debt on its books by trade credits with an implicit cost? I mean that higher implicit cost is just going to go under ‘raw material costs’, a head which seems impervious to further analysis in this context.

Taha, if the business is average i.e it does not possess any competitive advantage, then if there is a float, the default position of the analyst should be to assume that it comes with a cost.

To spot understatement of debt, simply look for unusual jump in trade credit/Revenue ratio combined with reduction in balance sheet debt. There should also be other signs such as a drop in interest expense but a contraction of EBITDA margin (because of implied interest). You will also see an unusual drop in working capital relative to size of revenues.

Slightly off topic: I highly recommend the 3rd edition of “Financial Shenanigans.” It has an absolutely marvellous chapter on “cash flow shenanigans” which I believe every fundamental investor should read. The other chapters are great too…

My understanding of a genuine float is that it consists of all those liabilities of a company that have no or negligible costs attached to it. If this is so, then most companies have atleast some float, and the only difference between companies is the quantum of that float relative to the total assets employed in the core business that generates that float.

So it’s interesting that you should say that if an average business has an apparent float, the default position of the analyst should be to assume that it comes with a cost. Because the implication of that would then be that an average business, on average, has only such trade creditors who build into their prices an implicit cost of extending say a 3 month credit on the goods they supply. And they thus have the scope to offer lower prices if the company offers them cash instead of taking goods on credit.

Which means that for the average business – on average –

1. Trade credit should not considered as a source of genuine float at all.

2. Debt is understated by the amount of trade creditors.

3. The only way to really be sure that normal trade credit doesn’t have a cost attached to it and is indeed a genuine source of float for a particular company is that if its current liabilities exceed its current assets (or negative WC). For a company will not mind this excess of current liabilities only if any or all of them truly do not have any cost attached to them.

4. The working capital requirements of an average business should actually be calculated without subtracting entries like trade creditors as they are in fact just another form of debt taken on to fund business assets.

Quite important considering that the vast majority of all businesses are average businesses.

Taha, recall that if most companies, as you wrote, have at least some float (trade credit) which comes at a cost, they also have receivables on the other side of the balance sheet which are the inverse of trade credit. For providing trade credit to its customers, the company will charge a slightly higher price than it would from a customer who will pay cash down. The difference between these two prices would be the implied interest on financing provided.

When an average business (with little, if any, market power) has both receivables and trade credit, then for an analyst to treat the normal quantum of trade credit as debt would be inappropriate because, in effect, it’s offset by receivables. However, if a company uses much larger amounts of trade credit, especially to camouflage it’s interest-bearing debt, then the analyst should mentally reverse that transaction and count the excess as debt. I know there is no precise way of doing this and different analysts will come up with different estimates of “debt camouflaged as trade credit”, I would still go ahead and do the job.

Thanks for asking.

[…] Fundoo Professor-Presentation On Moats And Floats. […]

Reblogged this on No Mean Sum and commented:

I can’t say enough about this presentation. Something many have pointed to but heretofore never presented so coherently.

good evening.

floats are a great metric to measure business moats. however, do you believe they are a better metric(or any way supererior) than say ROCE/profit margin/FCF or a combination thereof? Given that the later subset are far easier to obtain.

some dis-adv i can think of with floats

a) there are false positives i.e. sometimes floats can be intrinsic in the industry ( insurance, exhibition business).

b) this metric wouldnt bring up great businesses with great wide moats(eg. google).

-rishi

p.s. in one of the posts above you mentioned about a case of a company with negative reported equity and offered to share the details. is that offer extendable?

I agree. While the presence of large, free floats indicates the presence of a moat, the reverse is not necessarily true. However, I feel that measuring the cost and size of float (relative to assets and revenues) as well as its trend over time, is a good way to monitor fundamental changes taking place in a business over time.

I just sent you the case study.

i was recently going though the annual report of ibersol and thought of this posts. and thought you also might find it interesting(given the valuation).

http://www.ibersol.pt/ibersol/relatorio_ibersol2011/uk/index.html#/194/zoomed

—

in one of you earlier posts you mentioned “winner take all” businesses. i can only think of (a) industries that require high capex (in relation to total market size) that limits the players and (b) technology platform companies which have network effects. the former seems more sustainable than the later over the long term. are there any other rules of thumb that can be used to analyse such dynamics?

Thanks Prof for uploading this unique presentation on the value and impact of Float.

You have been able to make us see float in a new way

Can you please comment on the real estate industry in India . They are cash strapped and have huge debts .They take take large cash advances from customers but give huge discounts – so can I assume this is NOT an example float

From your presentation, Float generally means cost free funds

Rakeshg

Residential real estate business in India largely runs on float. Projects are launched, money from future home owners is taken, then the construction is done from that money. As an exercise, compare Ashiana Housing, Sunteck Reality, and Oberoi Realty with DLF.

Why is Ashiana largely debt-free but DLF is debt-laden? Is Ashiana’s float cost free? How important is that source of funding for the company? What will happen if it was not there?

Similarly look at Sunteck and Oberoi Realty. What’s unique about Ashiana, Sunteck, and Oberoi which is missing in DLF and Unitech and a whole lot of other real estate firms in India?

Hi Prof. Bakshi,,

Amex case is interesting one.

I had put down similar argument on Manappuram Gold finance when RBI was holding gun at heads of gold lending institutions at http://value-search.blogspot.in/ .

Request you to give your opinion on the argument presented at the mentioned blog. Would mean a lot to a novice value debutant 🙂

I would humbly mention that this is not an attempt to spam your much beloved and revered blog.

Regards,

Sarang

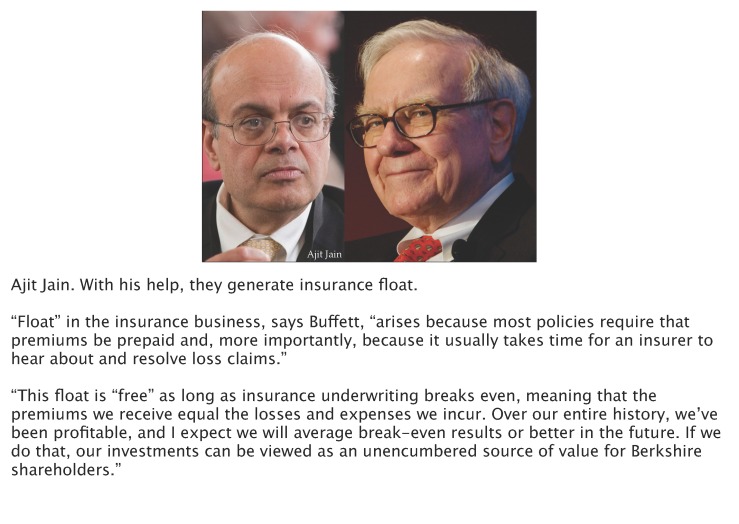

[…] In this way, Blackbaud’s deferred revenue is similar to the insurance float that has fueled much of Berkshire Hathaway’s gains. “Over the last 45 years, Berkshire’s insurance float enabled the company to effectively borrow huge amounts of cash, with no set repayment date, and with no tangible collateral put up. Even more astonishing is the fact that this money costs Berkshire less than nothing,” wrote Professor Bakshi in an excellent presentation on floats and moats. […]

[…] kan starkt rekommendera Sanjay Bakshis presentation ”Floats and Moats” vilket är ett fantastiskt arbete som detta stycke till stor del baserats […]

[…] Click Here for the Presentation […]

Prof bakshi,

It’s interesting how buffett’s mix of float is changing over time. It seems the key driver of float now comes from deferred taxes on the capital intensive businesses rather than insurance. I think this article could be great compliment to your work on floats and moats http://goo.gl/zvUv3w .

Regards,

Shreyas

[…] The research is a complimentary addition to the work on Floats and Moats by The Fundoo Professor […]

So buffett is now getting into car dealerships… Which have significant bailment/floorplan finance to fund the vehicle inventories. These revolving liabilities appear more like trade payables than debt. They are enduring, will grow and while they are not costless they are still a cheap source of financing. The problem is the funds are somewhat restricted and tied up to fund inventory, and cant be invested elsewhere. I would categorise this overall as low quality float.

With buffett flagging more dealership acquisitions in the future, how do you think dealerships tie into the float story? Do you think float is not a relevant factor in car dealerships or is high quality float simply too hard to acquire now?